Where Have All the Green Dots Gone?

Reflecting on our framework for public cloud company success.

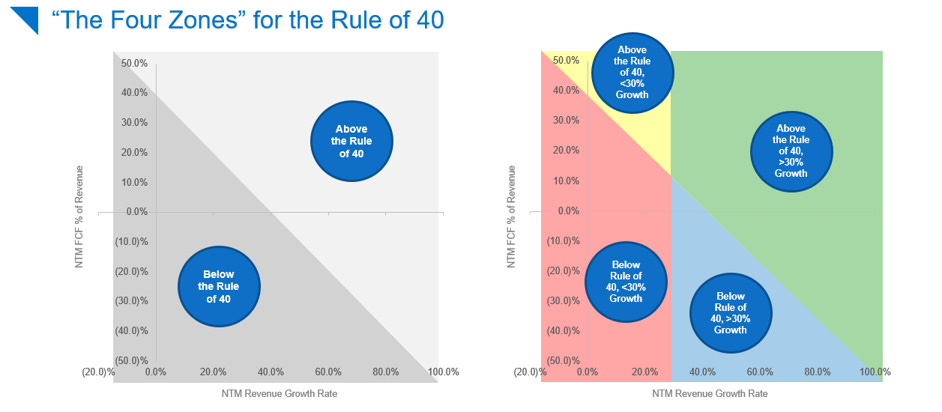

The “Rule of 40” is a popular financial metric positing that a SaaS company’s combined growth rate and profit margin should exceed 40%. It's a fine metric, but, by definition, it weighs growth and profitability equally. In different environments, investors may view the growth/profitability balance quite differently.

So, in 2019, we introduced the concept of the “Four Zones” of the Rule of 40, in which companies are grouped according to: 1) whether they meet the Rule of 40; and 2) whether they’re on track to achieve 30% NTM revenue growth. This process allowed us to track investor sentiment on profitability vs. growth in real time.

Typically, younger, faster-growing cloud companies found themselves in the Blue Zone, while best-in-class companies resided in the Green Zone. Established high-performers occupied the Yellow Zone, and companies that were below Rule of 40—while also not growing quickly—were relegated to the Red Zone.

Since we started this analysis, a majority of public cloud companies we track have resided in the Red Zone, but the other zones were well populated. In our original report published May 2019, there were eight Green Zone companies and ten Blue Zone companies.

By 2021, there were fourteen Green Zone companies and twenty-six Blue Zone companies.

Today, there is only one Green Zone company (Crowdstrike) and one Blue Zone company (SentinelOne)!

Rerunning these numbers forced us to reevaluate our approach to how we approach these zones. After all, we’ve been using this framework as a guide for our late-stage companies who are seeking to understand the tradeoffs between growth and profitability and how the market is valuing companies across that spectrum. Being a Green Zone company has always been aspirational, but we contemplated whether it was now an impossibility. Is the framework we’ve been presenting for the last five years unrealistic for the cloud companies of 2024?

In a word, no. Here is how we think about this:

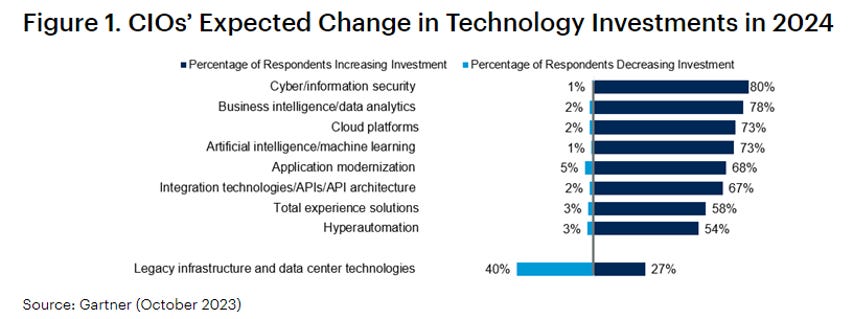

The primary catalyst behind this market change is rising interest rates. As the cost of capital increased, companies faced tighter budgets (both software buyers and software companies themselves), which slowed growth projections. We see strong early signs that software budget will bounce back in 2024 (see Gartner), with pipeline, sales cycles and close rates all starting to improve.

Cloud companies today primarily monetize by pricing per seat. We saw a wave of seat contraction in the past year, with companies across industries going through headcount reductions and doing a “cleanup” of seats they didn’t believe they needed to be paying for (i.e. low usage/low value seats). It is hard to say if the major headcount reductions are entirely behind us – we certainly hope that the market took the majority of that pain last year – but from our vantage point, we feel confident that the majority of “seat cleanup” is done.

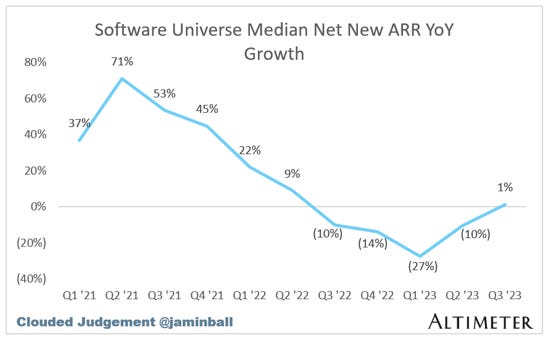

A leading indicator we track is the trend in year-over-year, net-new ARR add, which investor Jamin Ball does a great job tracking in his Clouded Judgement Substack. Year-over-year ARR add had been <0% for four quarters but is back in the black as of Q3 ’23.

Between 2022 and 2023, the SaaS IPO landscape changed dramatically. In 2021, there were twenty-seven SaaS IPOs added to our index, but during the following two years, only Klaviyo went public. We posit that both the Blue and Green Zones harbor a non-negligible number of "sleepers" – companies that have refrained from IPOs due to the market correction that began in 2022. For instance, Cribl recently announced crossing $100M in annual recurring revenue (ARR) in under four years, while Databricks* reported exceeding $1.5B in ARR, growing at a remarkable 50%. As we approach 2024 and 2025, we anticipate that new IPOs will repopulate these zones, as they have in previous years.

For these reasons – software budgets returning, less downward pressure on seat retention and a re-opening of the IPO window – we believe that our Blue and Green Zones will eventually be repopulated again, and this Four Zones framework will continue to be a strong one for late-stage private and public cloud companies to use.

There is one more key point worth making: A “Red Zone” company today looks very different from a Red Zone company in 2021.

Look at the dots in the red zone. See the migration up? The market compelled public companies to strive for positive free cash flow, and most have been able to make it there. You can look at the 2023 chart and only see the compression on the X-axis to the left, but the compression of the Y-axis up is just as notable in our eyes. The median public company today is achieving higher profit margins and is in a healthy position to leverage its newly established operating leverage to reaccelerate growth if and when investors place greater value on growth.

Irrespective of whether the SaaS industry experiences a resurgence in 2024 or beyond, we believe it is crucial to maintain the stability of our existing frameworks, despite recent shifts in fundamental performance and valuation metrics.

In our venture investments, we continue to seek out companies that align with the T2D3 framework we introduced in 2015, emphasizing initial traction followed by rapid growth (Triple, Triple, Double, Double, Double). In the public markets, we eagerly await the reopening of the IPO window, offering opportunities for innovative, younger companies to join our index, while existing public companies can leverage their newly established operating leverage to reaccelerate growth.

*Denotes a Battery portfolio company. For a full list of all Battery investments, please click here.

The information contained herein is based solely on the opinion of Neeraj Agrawal, Brandon Gleklen and Jack Mattei and nothing should be construed as investment advice. This material is provided for informational purposes, and it is not, and may not be relied on in any manner as, legal, tax or investment advice or as an offer to sell or a solicitation of an offer to buy an interest in any fund or investment vehicle managed by Battery Ventures or any other Battery entity.

This information covers investment and market activity, industry or sector trends, or other broad-based economic or market conditions and is for educational purposes.

The information and data are as of the publication date unless otherwise noted. Content obtained from third-party sources, although believed to be reliable, has not been independently verified as to its accuracy or completeness and cannot be guaranteed. Battery Ventures has no obligation to update, modify or amend the content of this post nor notify its readers in the event that any information, opinion, projection, forecast or estimate included, changes or subsequently becomes inaccurate.

| A guest post by

|

| A guest post by

|